Announcement: Valutico Provides an Easier Way to Value Startups

-

New Venture Capital (VC) method allows faster valuations of mid- to late-stage startups

Valutico has once again made finance professional’s lives easier by announcing the launch of the Venture Capital (VC) method for valuing start-ups, available for the first time within its online platform.

Although there are more than 4,000 active VC firms globally, valuing start-up companies remains problematic because traditional valuation methods don’t always work. Valutico’s team has developed an online solution that incorporates data from over 50,000 peer companies, and hopes to help overcome this issue faced by valuation professionals around the world.

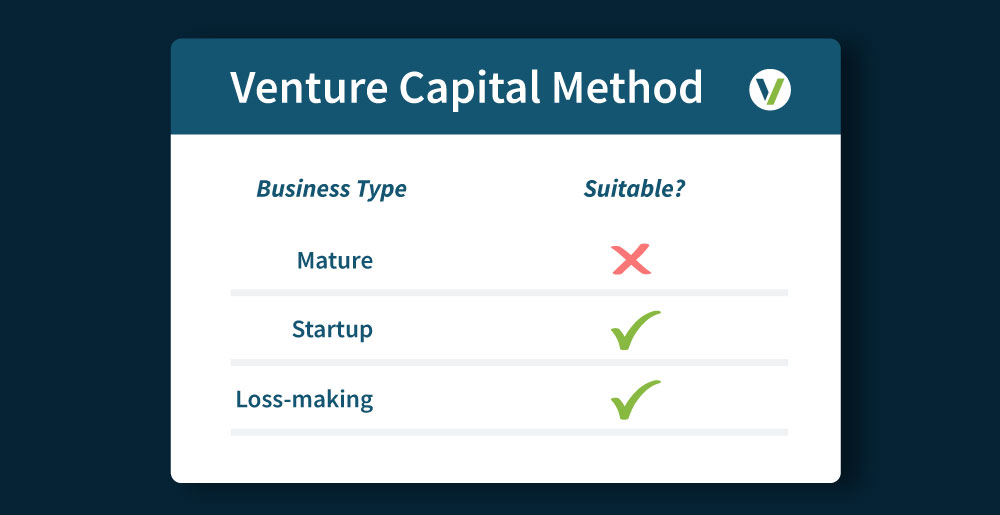

As some recent start-up valuations are falling amidst investor caution, this new development comes at an opportune time to positively impact how effectively financial firms value young businesses. Already helping more than 450 financial firms perform over 10,000 valuations each year, Valutico’s new development also opens the door for valuing loss-making businesses, for which the VC method is also apt.

CEO of Valutico, Paul Resch stated:

“We’re extremely excited to announce the new VC method as part of Valutico’s ever-expanding toolbox. We’re particularly happy that this represents a significant increase in our offering for Venture Capital and Corporate Finance firms across the 70 countries Valutico is already being used in. With all the calculations and relevant data in one place, the VC method will help make these types of mid- and late-stage start-up valuations much easier.”

One difficulty with valuing start-ups is that they have less financial history behind them. In contrast to other techniques, the VC method focuses instead on the VC firm’s desired rate of return as a key component of the valuation, and so allows new businesses that may still be loss-making, to be valued more effectively than with traditional methods such as a discounted cash flow (DCF).

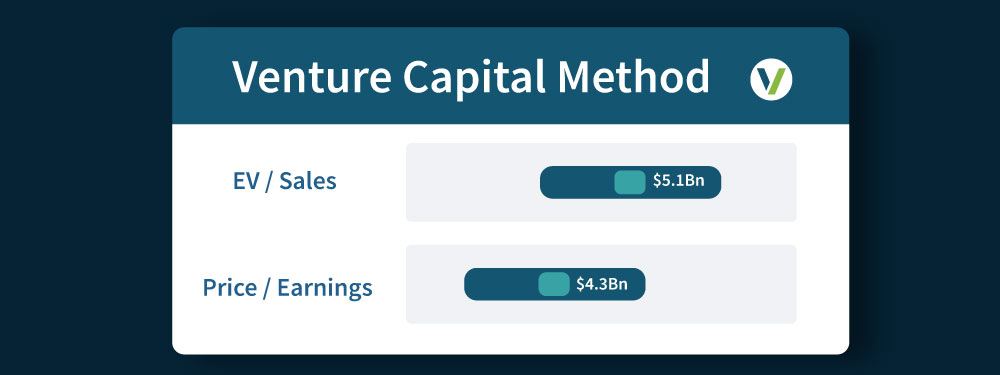

VC firms invest in start-ups to gain a return on their investment, whereas M&A and Corporate Finance firms are interested in valuing new businesses with growth potential for a wide range of reasons. With Valutico’s new development, practitioners can quickly perform a VC valuation based on EV/Sales, EV/EBITDA, EV/EBIT and P/E multiples as a useful addition to other research on the company and the industry. With a highly active start-up sector even within an uncertain economic climate, valuing new businesses remains a vital task for a wide range of finance professionals.

For demonstrations please contact Head of Marketing, Alex Harris.

Have Questions About the VC Method?

What is the VC method?

The Venture Capital (VC) method is an assessment for valuing start-up and high growth businesses. It is based on the company’s projected earnings at a certain future date, taking into account the money multiple and associated rate of return the investor would like to earn on their investment, assuming they will exit the investment at a specified future date.

The VC method calculates the exit valuation at the specified future date by applying the observed multiples (EV/Sales, EV/EBITDA, EV/EBIT and P/E) of comparable listed companies and comparable transactions to the target company’s future earnings.

Taking this exit value into account, it then determines the price at which the investor can invest today in order to achieve their target money multiple and associated Internal Rate of Return (IRR).

How does the VC method work?

The default multiple is the average of the median of the comparable listed companies and the median of the comparable transactions. The default multiple can be overwritten by the user within the Valutico platform.

The default time horizon is 5 years, which can also be overwritten by the user. The chosen multiple is applied to the target company’s forecast earnings at the chosen forecast year to determine the exit value.

The user is also required to specify a money multiple that an investor will require over the specified time horizon. The money multiple determines the IRR, which is used as the discount rate to discount the exit value and arrive at the valuation (as of the valuation date).

Will this value early-stage start-ups?

While the VC method can be used to value early-stage start-ups, it is not often the preferred approach due to the significant uncertainty attached to the forecast cash flows resulting in very high money multiples and IRRs required to compensate the investor for such risk.

How accurate are the valuation figures?

It’s notoriously difficult to value new businesses accurately, and any method is fraught with some uncertainty. However, using a method like the VC method does provide a systematic way to arrive at a valuation range, and so it represents a useful tool to produce a figure that takes account of the perception of risk, the expected return, the projected earnings, and similar peer companies.

Is the Valutico platform suitable for VC investors?

If you use Valutico regularly, either to perform valuations on multiple companies, or to update or iterate multiple valuations, then Valutico can be extremely helpful because of how it speeds up this time-intensive process.

How are the calculations performed?

The Entry Value (EntV) is calculated by discounting the Exit Value (ExV) at the specified future year (t) at the IRR, as follows:

EntV = ExV(1+IRR)t

What data is used for the companies ‘comps’ comparisons?

We use different leading providers of public and private company data to come up with our expectations for reasonable exit multiples.

What are the limitations of using a traditional method like a DCF to value a new business?

While the DCF also discounts future cash flows to a present value today, it does so using discount rates typically calculated using the Capital Asset Pricing Model (either Weighted Average Cost of Capital (WACC) or Cost of Equity (CoE)). The calculation of these discount rates are based on the observed betas of similar listed peer companies. These companies, being listed, are mostly large, mature companies which means that the WACC that is calculated is normally very low (reflecting the lower risk of large, listed companies compared to the start-up in question).

For growth or mature SMEs, this discrepancy between the WACC of listed vs private companies is accounted for with a Cost of Equity Premium. The CoE Premium is meant to capture the additional risk between the peer group of listed companies and the target company. When valuing startups, the challenge is that, in order to arrive at a realistic valuation, the CoE Premium can become very large (sometimes resulting in a doubling or even tripling of the original WACC).

It can therefore be a much simpler analysis to do away with the WACC as a discount rate and focus on the IRR of what a potential investor would like to achieve when making a VC or early stage investment.

Which parameters can I change in the VC method in Valutico?

You have control over the time horizon for which you are interested in this business, the amount of return you would expect to make over the entire time period, which ultimately determines the expected investor Internal Rate of Return (IRR), as well as full control over every exit multiple: EV/Sales, EV/EBITDA, EV/EBIT, and P/E.

Did Valutico invent this method?

As much as we would love to take credit for it, the Venture Capital method was developed by Harvard Business School Professor Bill Sahlman in 1987.

Is it worth purchasing Valutico just to use the VC method?

We recommend subscribing to Valutico if you regularly value businesses, and you want to save yourself time by having easy access to a tool that speeds up the process of accessing relevant data, and exporting reports instantly. However, if you only do one or two valuations a year, and you’re interested in a once-off valuation, you can reach out to our valuation services team who support our clients by providing once-off valuations.

If you want to learn more about the VC Method, book your demo here.